Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv 60 Minutes on CNBC CNBC November 11, 2012 11:00pm-12:00am EST

11:00 pm

[stopwatch ticking] >> besides the president, bernanke is the most powerful man working to fix the economy. and we were surprised by his candor. mr. chairman, i'm gonna start with a question that everyone wants me to ask. when does this end? [stopwatch ticking] >> no one comes in without f.d.i.c. badges. >> could your bank be shut down? that's what's happening to this bank and to banks across the country. it's being done in secret by a group of agents led by the f.d.i.c., who move in after closing time when a bank has failed. [stopwatch ticking] >> it's weird economics when it really comes down to it, isn't it? >> well, from our perspective at the united states mint, it's unsustainable. you can't sustain losses on pennies and nickels and expect to be a viable organization that

11:01 pm

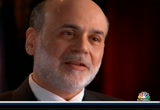

benefits the american people. >> welcome to 60 minutes on cnbc. i'm leslie stahl. by most accounts, the financial crash of 2008 pushed the u.s. economy to the brink of collapse. in its aftermath, some of the country's biggest banks received very big bailouts while large numbers of small local banks failed. this edition features a unique inside look at the seizure of a failed bank and a rare interview with one of the men at the center of the 2008 economic crisis and the recovery plan that has followed, the chairman of the board of governors of the federal reserve system, ben bernanke. plus, morley safer asks, "can america afford the lincoln penny?" well, we begin with bernanke. after the crash of '08, bernanke invoked emergency powers, and with unprecedented aggressiveness, he's thrown more than $1 trillion at the crisis.

11:02 pm

the words of any fed chairman cause fortunes to rise and fall, and so by tradition, chairmen of the fed do not do interviews. that is, until march of 2009 when ben bernanke sat down with scott pelley. >> mr. chairman, i'm gonna start with a question that everyone wants me to ask. when does this end? >> it depends a lot on the financial system. the lesson of history is that you do not get a sustained economic recovery as long as the financial system is in crisis. now, we've seen some progress in the financial markets, absolutely, but until we get that stabilized and working normally, we're not gonna see recovery. >> i wonder, do you expect double-digit unemployment? >> well, it's hard to forecast exactly where we're going. unemployment is rising. job losses are still very severe. and, no doubt, the unemployment rate's gonna go higher than it is. but i think, again, that if we do succeed in stabilizing the

11:03 pm

financial system, that we'll begin to see a slower pace of decline and eventually a stabilization that will set the basis for a recovery. >> ben bernanke, age 55, has been chairman of the federal reserve board since 2006. for our interview, he opened up the fed headquarters, rarely seen by the public. it's a monumental building along the national mall. construction started in 1935, in the depths of the great depression. you know, mr. chairman, i think the federal reserve, for most people, is a mystery. >> well, it's an institution that people don't hear so much about, but it's a very important one. it manages monetary policy for the country. it's one of the main tools we have for stabilizing our economy and keeping prices stable. >> when was it founded? >> the fed was created by congress in 1913, and its original purpose was to deal with financial panics, which is what we're doing right now. >> bernanke's crisis started in

11:04 pm

2007 with the mortgage meltdown. lenders began to fail. bernanke cut interest rates repeatedly. in 2008 the fed stopped the collapse of bear stearns by arranging a sale to another firm, but then came the end of wall street as we knew it. mortgage giants fannie mae and freddie mac were seized by the government. on september 14th, merrill lynch was sold in distress, and the next day, 158-year-old lehman brothers failed. you didn't rescue lehman brothers. it set off a worldwide panic when it went bankrupt, and i wonder, looking back, whether you think that was a mistake. >> there were many people who said, "let them fail. you know, it's not a problem. the markets will take care of it." and i think i knew better than that, and lehman proved that you cannot let a large internationally active firm fail in the middle of a financial crisis. now, was it a mistake? it wasn't a mistake for the following reason. we did not have the option. we didn't have the tools.

11:05 pm

the federal reserve cannot put capital into an institution. all we can do is make loans against collateral. >> the day after lehman, bernanke's fed did something astounding. it loaned $85 billion to a company that wasn't a bank at all, american international group, the global insurance giant that was also involved in backing risky mortgage investments. bernanke says unlike lehman, the fed could make the loan based on good collateral in a.i.g.'s portfolio. there have now been four rescues of a.i.g. for about $160 billion. why is that necessary? >> let me just first say that, of all the events and all the things we've done in the last 18 months, the single one that makes me the angriest, that gives me the most angst, is the intervention with a.i.g. here was a company that made all

11:06 pm

kinds of unconscionable bets. then when those bets went wrong, they had--we had a situation where the failure of that company would have brought down the financial system. >> you say it makes you angry. what do you mean by that? >> it makes me angry. you know, i slammed the phone more than a few times on discussing a.i.g. it's just absolutely-- i understand why the american people are angry. it's absolutely unfair that taxpayer dollars are going to prop up a company that made these terrible bets, that was operating out of the sight of regulators, but which we have no choice but to stabilize or else risk enormous impact, not just on the financial system but on the whole u.s. economy. >> by september, bernanke and former treasury secretary hank paulson went to capitol hill to urge a massive bailout of the banking system. >> at that period, i thought we were pretty close to a global

11:07 pm

financial meltdown. >> how much danger was there? how close a call? >> it was very close. it was very close. we--the congress passed the bill that gave treasury the right to put capital into the banks in the first week of october, and it was in the second week of october that the crisis reached its peak. and if we had not had those powers, we could have had a much, much worse outcome. so it was a very dangerous situation. >> that second week of october, the dow fell 18%, its worst week in history. in the midst of the crisis, bernanke had freedom to act immediately. he doesn't need prior permission from congress or the president. while they debated on capitol hill, bernanke cut interest rates nearly to zero, then he used depression-era emergency powers to launch a dozen rescue programs of his own. there was support for money market funds, mortgages, short-term lending to small businesses, and support for auto

11:08 pm

loans, student loans, and small business loans-- commitments of $1 trillion, doubling the size of the fed's balance sheet. is that tax money that the fed is spending? >> it's not tax money. the banks have accounts with the fed, much the same way that you have an account in a commercial bank. so to lend to a bank, we simply use the computer to mark up the size of the account that they have with the fed. so it's much more akin, although not exactly the same, but it's much more akin to printing money than it is to borrowing. >> you've been printing money? >> well, effectively, and we need to do that because our economy is very weak and inflation is very low. when the economy begins to recover, that will be the time that we need to unwind those programs, raise interest rates, reduce the money supply, and make sure that we have a recovery that does not involve inflation. [stopwatch ticking] >> coming up, ben bernanke is doing things with the federal reserve that have never been done before.

11:09 pm

>> it's an extraordinary time. this is a chance for me, i think, to talk to america directly. >> when 60 minutes on cnbc returns in a moment. if we want e our schools... ... what should we invest in? maybe new buildings? what about updated equipment? they can help, but recent research shows... ... nothing transforms schools like investing

11:10 pm

in advanced teacher education. let's build a strong foundation. let's invest in our teachers so they can inspire our students. let's solve this. [ female announcer ] there's one thing dave's always wanted to do when he retires -- keep working, but for himself. so as his financial advisor, i took a look at everything he has. the 401(k). insurance policies. even money he's invested elsewhere. we're building a retirement plan to help him launch a second career.

11:11 pm

dave's flight school. go dave. [ male announcer ] when the conversation turns to finding a financial advisor who's fully invested in you, turn to us. wells fargo advisors. together we'll go far.

11:12 pm

>> the fed issues u.s. currency. that's why it says, "federal reserve note," on all the bills in your wallet. this is the bureau of engraving and printing just a few blocks from bernanke's office. the fed's mandate from congress is to put enough money in the system for maximum employment but not so much that it sets off inflation. the fed actually pays for itself and returns billions in profits to the treasury. in a sense, bernanke has been preparing for this emergency his whole professional life. he got a phd in economics from m.i.t., he chaired the economics department at princeton, and his specialty is the great depression. he's among many economists who

11:13 pm

now believe that it was the federal reserve itself that helped turn a recession in 1929 into a global calamity. >> they made two mistakes, basically. one was, they let the money supply contract very sharply. prices fell, deflation. so monetary policy was, in fact, very contractionary, very tight during that period. and then the second mistake they made was, they let the banks fail. they didn't make any strong effort to prevent the failure of thousands of banks. >> bernanke told us that we were close to a second depression, and he is determined not to let the major banks fail on his watch. you know, mr. chairman, there's so many people outside this building, across this country, who say, "to hell with them. they made bad bets. the wages of failure on wall street should be failure." >> let me give you an analogy, if i might. if you have a neighbor who smokes in bed and he's a risk to everybody, and suppose he sets fire to his house, and you

11:14 pm

might say to yourself, "you know, i'm not gonna call the fire department. let his house burn down. it's fine with me." but then, of course, what if your house is made of wood and it's right next door to his house? what if the whole town is made of wood? well, i think we'd all agree that the right thing to do is put out that fire first and then say, "what punishment is appropriate? how should we change the fire code? what needs to be done to make sure this doesn't happen in the future? how can we fireproof our houses?" that's where we are now. we have a fire going on. >> it's still burning. >> it's still burning. >> are you committing, in this interview, that you are not going to let any of these banks fail, that no matter what their balance sheet actually looks like, they are not gonna fail? >> they are not gonna fail, but what we can do, should it be necessary, is try to wind it down in a safe way. >> in other words, bernanke thinks government should stabilize failed financial companies and take them apart slowly. what are the dangers now? what keeps you up at night? >> the biggest risk is that, you know, we don't have the

11:15 pm

political will, we don't have the commitment to solve this problem and that we let it just continue, in which case, you know, we can't count on recovery. >> the seal of the federal reserve is embedded in the floor just outside the room that changes the fortunes of the world. wow. they don't build them like this anymore. this is where bernanke meets with his six fellow governors of the federal reserve, all of them appointed by the president of the united states. bernanke also chairs the federal open market committee, which decides interest rates. when i called and proposed this interview about a year ago, your representative laughed out loud and said, "the fed chairman never does an interview." i wonder, why are you doing this? >> well, it's an extraordinary time. it's an extraordinary time. this is a chance for me, i think, to talk to america directly. >> and a chance for us to

11:16 pm

understand where he comes from. [rail crossing bell dinging] ben shalom bernanke grew up in one of the few jewish families in dillon, south carolina, today a town of about 6,000 people. his grandfather jonas immigrated from eastern europe, landed at ellis island, and came here to start a drug store. >> our family came here in 1941. my grandfather, jonas bernanke, bought this building, made it into the jay bee drugs, after his initials. >> later, his father and uncle took over the store, which has since become a restaurant. we're sitting on this corner where your family's store was, and i see it's main street. >> yes. >> people feel like guys like you are tuned in to what happens on wall street and you forget places like this. >> you know, i come from main street. that's my background. and i've never been on wall street. and i care about wall street for one reason and one reason only, because what happens on wall

11:17 pm

street matters to main street, and if we don't have stabilization in the financial markets, if we don't take the steps necessary to make sure that credit is flowing again, then my father couldn't get a loan to build his new store. when i was young, we had just a screen porch over here on the left side. >> we went to the old neighborhood. the bernankes left here years ago, and a recent owner couldn't quite make the mortgage, so the economy literally hit home. when you first heard that your childhood home had gone into foreclosure, what did you think? >> well, i was sorry to hear it, but, you know, in a way, i wasn't surprised. dillon has taken, you know, a pretty big hit in the economic downturn. the unemployment rate is about 14%, and there have been a good number of foreclosures and plant closings and those things, and i think about that. >> numbers were always bernanke's thing. he taught himself calculus and got an s.a.t. score of 1590

11:18 pm

out of 1600. a friend talked him into aiming high for college. >> i came home from school one day and there was a phone call for me, and i picked up the phone. they said, "this is the harvard admissions department. we'd like to let you know that you're accepted in the freshman class." and i said, "come on, who is this really?" and but my parents had their doubts about my leaving and going so far from home. >> no, wait a minute. your parents weren't thrilled that you were going to harvard? i mean, this is a dream come true. >> my mother was definitely against it. first of all, she said, "you know, you don't have the clothes. you won't be able to dress properly for harvard. and it's a long way from here. how are you gonna come home at holidays, and so on?" so my parents ate into their savings to let me go, which i'm always grateful for. >> bernanke helped pay for college working construction and working here. the future chairman of the fed wore a poncho and waited tables at south of the border. what did you learn about work? >> work is hard. in order to feed your family

11:19 pm

and to give your kids opportunities, it's not an easy thing. >> back in the marble confines of the federal reserve, bernanke told us that he understands that many americans are afraid. i've been kicking around the country. i spoke to a woman in ohio who took her son out of college because she got laid off. i spoke to a woman in nevada who has an advanced stage of cancer, and she was told by her county hospital that they couldn't treat her because a hold had been blown in the state budget. what do you say to those people? >> well, i got into economics because i wanted to make things better for the average person. when i see a job loss number of 650,000, like we saw last month, i know that's not just a number. that's 650,000 lives that have been disrupted, families that have had to move or take children out of school, houses that may be in danger of foreclosure. i know something about what

11:20 pm

people are going through. >> and that makes it all the more outrageous when he hears of financial firms handing out perks and bonuses after they've taken bailout money. >> the era of this high living, this is over now, and that they need to be responsible and use the money constructively. >> and you would say what to those bankers right now in this interview? i'd say that their job right now is to find a way to make loans to creditworthy borrowers, to get their banks back on the path of making good loans, safe loans, and to have a reasonable sense of humility based on, you know, what's happened in the last 18 months. [stopwatch ticking] >> coming up... >> how do we prevent this from occurring another time? >> tougher regulation of large firms. >> next when 60 minutes on cnbc returns.

11:21 pm

up. a short word that's a tall order. up your game. up the ante. and if you stumble, you get back up. up isn't easy, and we ought to know. we're in the business of up. everyday delta flies a quarter of million people

11:22 pm

while investing billions improving everything from booking to baggage claim. we're raising the bar on flying and tomorrow we will up it yet again. if you are one of who have used androgel 1%, there's big news. presenting androgel 1.62%. both are used to treat men with low testosterone. androgel 1.62% is from the makers of the number one prescribed testosterone replacement therapy. it raises your testosterone levels, and... is concentrated, so you could use less gel. and with androgel 1.62%, you can save on your monthly prescription. [ male announcer ] dosing and application sites between these products differ. women and children should avoid contact with application sites. discontinue androgel and call your doctor if you see unexpected signs of early puberty in a child, or, signs in a woman which may include changes in body hair or a large increase in acne, possibly due to accidental exposure.

11:23 pm

men with breast cancer or who have or might have prostate cancer, and women who are, or may become pregnant or are breast feeding should not use androgel. serious side effects include worsening of an enlarged prostate, possible increased risk of prostate cancer, lower sperm count, swelling of ankles, feet, or body, enlarged or painful breasts, problems breathing during sleep, and blood clots in the legs. tell your doctor about your medical conditions and medications, especially insulin, corticosteroids, or medicines to decrease blood clotting. talk to your doctor today about androgel 1.62% so you can use less gel. log on now to androgeloffer.com and you could pay as little as ten dollars a month for androgel 1.62%. what are you waiting for? this is big news. inspiration. great power. iconic design. exhilarating performance. [ race announcer ] audi once again has created le mans history!

11:24 pm

[ male announcer ] and once in a great while... all of the above. take your seat in the incomparable audi a8. take advantage of exceptional values on the audi a8 during the season of audi event. ♪ [stopwatch ticking] >> the federal reserve is the lifeblood of the banking system. its 12 regional banks are clearinghouses for commercial banks. this is one of the vaults associated with the reserve bank in new york. robots carry cash in the vault that is as big as a football field and four stories high. each pallet loaded with $100 bills is worth $64 million. the fed has 22,000 employees. it clears your checks and your atm withdrawals and provides economic forecasts. but one of its most important responsibilities is regulating

11:25 pm

the nation's biggest banks, to be the watchdog. you're supposed to keep them out of trouble, so how did all this happen? >> well, a lot of mistakes got made, no question about it, but, you know, this was a much bigger thing than any single firm or any single individual. over the last dozen years or so, enormous amounts of savings has flowed into the united states and some other industrial countries. that savings has come from china and east asia. it's come from oil producers. and it has--hundreds of billions of dollars has come into our financial system. and, you know, that would be great if we took that money and invested it wisely and got a high return. but instead, our financial system didn't do a good job. we had a regulatory system that was like a sand castle on the beach. when you had little small waves just lapping up against the sand castle, everything looked good, but when you had a big breaker come in, suddenly the system wasn't strong enough to deal with it.

11:26 pm

>> does the federal reserve bear any responsibility for missing what was happening to the banks as it was happening? >> well, like other regulators, we probably could have done more. we've already done a lot of-- put a lot of effort into reviewing our practices, into reviewing the banks' practices. we are trying to strengthen our regulation at every point that we can. so i don't want to deny that we certainly could have done a better job and others could have done a better job. >> how do we prevent this from occurring another time? >> well, tougher regulation of large firms. it includes having a set of laws that allows us to wind down a large internationally active firm without the adverse impacts on the markets that a disorderly bankruptcy would have. it includes possibly having a systemic regulator, a regulator that has some responsibility to look at the system as a whole. >> your response has been to do

11:27 pm

what the fed didn't do in 1929, and that is pour money into the system, but there's an argument made today that that's not what the problem is. the problem isn't that there's too little money in the system. the problem is, there's too much fear in the system, that with these companies being propped up by the government, no one on wall street can tell who's solvent and who's not, and therefore, business does not move. >> well, i absolutely agree that confidence is key. people don't know what's happening, and they're afraid, and they're not sure what-- you know, whether or not the system is gonna recover. so how do you get confidence? that's the question. and i think the way to get confidence is to show progress. >> but are you seeing any progress? what's going well? >> i think all of our efforts so far have produced results. we're buying about $500 billion in mortgages packaged in securities by the g.s.e.s

11:28 pm

fannie mae and freddie mac, and that seems to have brought down mortgage rates significantly, allows people to refinance, to get out of high-rate mortgages. we are seeing progress in the money market mutual funds and in the business lending area. and i think as those green shoots begin to appear in different markets and as some confidence begins to come back, that will begin the positive dynamic that brings our economy back. >> what will be the first signs of recovery? >> one sign would be that a large bank is successful in raising private equity. right now all the private money is sitting on the sidelines saying, "we don't know what these banks are worth. we don't know that they're stable." and they're not willing to put their money into the banks. >> if you had a message for the american people in this interview, what would it be? >> scott, i'd say three things. i'd say, first of all, that the federal reserve is here and is

11:29 pm

gonna do everything possible to support this recovery. the second thing i would say is that recovery is not gonna happen until the financial markets and the banks are stabilized, and we do have a plan. we have a program for that. but it's gonna take some patience. it's gonna take some support. and, you know, we're gonna have to go forward with that. but the third and final thing i'd just like to say to the american people is that i have every confidence that this economy will recover and recover in a strong and sustained way. the american people are among the most productive in the world. we have the best technologies. we have great universities. we have entrepreneurs. i just have every confidence that, as we get through this crisis, that our economy will begin to grow again and it will remain the most powerful and dynamic economy in the world. >> chairman bernanke is not the only person concerned about the state of the country's financial system. a lot of people are worried

11:30 pm

about their bank these days. while devastated giants like citigroup get bailed out again and again and again, many smaller banks are failing. the federal agency that takes over unsound banks is the federal deposit insurance corporation, the same people who guarantee that depositors won't lose their money. and you don't see the f.d.i.c. seizing banks, because these takeovers happen secretly at night to make sure that there's no needless panic by depositors. but in february 2009, scott pelley was given extraordinary access to one of these operations, because the f.d.i.c. wants you to see what happens to your money when your bank has failed. >> they're gonna start at one branch, pull the cash out, take it inside the bank. >> this is a team of f.d.i.c. agents preparing to seize a bank outside chicago. >> what we need to do is, we need to pull the corporate records. >> they've checked into this

11:31 pm

hotel under a fictitious name, cb and associates. to prevent a run on the bank, they don't want anyone to know who they are or why they're here. >> you all know that this is for the closing of heritage community bank. >> cheryl bates and arthur cook are in charge of the operation that has been given the code name "happy." strange, considering what they're about to do. >> do not discuss outside of this room what is going on, what we're here for. >> they're here to seize all five branches of heritage community bank, a 40-year-old illinois bank providing savings, student loans, mortgages, and checking. but like so many others recently, heritage made ruinous bets on real estate. sheila bair is chairman of the f.d.i.c. i wonder if you have a number in mind of how much the f.d.i.c. is prepared to pay for bank failures in 2009. >> well, we make a five-year projection that for the next

11:32 pm

five years we project that we'll lose $65 billion on bank closings. >> $65 billion? >> $65 billion. >> some of that was about to be spent on the immanent failure of heritage community bank. it held 12,000 deposits totaling more than $200 million. the f.d.i.c. team waited for the last customer to leave. cheryl bates prepared to go in. what sorts of specialists do you have on this team? >> we have accountants. we have asset specialists who specialize in loans. we have people who specialize in just the physical facilities. and we have a group of investigators that come in and do a review on the reasons for the bank failure. >> really, your whole team could come in and run the bank. >> yes. [stopwatch ticking] >> coming up, operation happy goes into effect. >> we're getting the bank personnel assigned with their f.d.i.c. counterparts, and then

11:33 pm

we have an investigations group that comes in and does a review of the bank. >> the seizure of heritage community bank next, when 60 minutes on cnbc returns.

11:36 pm

>> in october 2008, the f.d.i.c. and the state of illinois ordered the bank to stop risky lending and raise cash, but heritage couldn't find new investors. the night of february 27th, no one at the bank knew that the end was minutes away. the f.d.i.c. walked into all five branches at once. the chief executive, john saphir, was told that the bank that was his life's work was no longer his. we waited outside as they delivered the news to the employees. >> with heritage bank, your pay stopped at 6:00 p.m. at 6:01 you went on a pay which is paid by the f.d.i.c.

11:37 pm

unused vacation time, you will be paid for it. you will not lose it. >> in that moment, operation happy looked pretty grim. >> when we walk in, we appear to be the bad guy. >> i mean, some of those people had been there more than 20 years. >> and those are the ones who take it the hardest, because they feel that they have put their life into it and now it's no longer there. >> make sure that no one comes in without f.d.i.c. badges. >> the employees now work for the f.d.i.c. a public notice went up, and that was the signal to a team of nearly 80 people to take over the bank. they took control of the bank website and added a notice that all deposits were safe. then they started an inventory of all the assets and liabilities. what's happening right now? >> we're getting the bank personnel assigned with their f.d.i.c. counterparts. the accounting people are meeting with our accounting managers. and then we have an investigations group that comes

11:38 pm

in and does a review of the bank. >> they broke the news to the media and prepared to reopen the bank saturday morning as usual. what do you expect from the customers? >> i think the customers, some of them will come in with a sense of fear. >> fear created the f.d.i.c. in 1933, after the depression set off panics that wiped out even healthy banks. >> we've been around for 75 years and nobody's ever lost a penny of insured deposits. >> no depositor has even lost a penny since the f.d.i.c. went into business? >> that's right, of insured deposits. that's absolutely right, which is why you need to make sure you're below the insured deposit limits. but no, no one's ever lost a penny. >> and the insured deposit limit is what? >> right now it's $250,000. that's the base limit. >> at what point is the f.d.i.c. broke? >> the f.d.i.c. is backed by the full faith and credit of the united states government. so we if we need to--we try not to and don't want to--but if we need to, we can borrow from treasury to make up for any shortfall. >> so the f.d.i.c. never goes broke? >> we don't go broke. no, we are the government. we're backed by the full faith and credit of the united states government.

11:39 pm

>> many depositors were worried when the bank reopened on saturday. >> morning. >> the f.d.i.c.'s ricky mccullough stood at the door. the people who were coming in this morning, what were they asking you? >> "can i still write checks?" "can i access my safety deposit box?" "can i use my atm machine?" >> and to all those questions, you answered what? >> "yes." >> customer bill hess showed up on a mission with an empty briefcase. he intended to leave with all of his money. >> we'd be glad to answer any questions for you. >> i don't care anymore. >> he said, "i don't care anymore." >> and so i became a little concerned, so i came inside, and one of the things that he told me as he opened up his briefcase, he said, "well, i don't have a gun in here." so i said, "well, that's good." >> mccullough explained to hess and his wife, audrey, that their savings were safe. >> so if you have a single account, that's $250. if you have a single account, that's $250, so now that's $500. >> hess' briefcase was empty when he came in and empty when he came out. >> we just thought we were gonna see "closed" and the doors

11:40 pm

locked, you know. >> so how do you feel now that you've talked to them? >> it's fine. >> assured, assured. >> you feel assured? >> yes, yes. >> you had confidence in the f.d.i.c. >> right, yeah. now, if they can't pay you, then i won't have confidence in them either. [laughter] >> there are three ways the f.d.i.c. takes over a bank. it can close it and pay off depositors, run the bank itself, or, more often, it'll try to find a buyer. >> we do have bids from five different parties. >> a few days before the takeover of heritage community bank, we were at the f.d.i.c. office in dallas, where they were holding a secret online auction in hopes of finding a buyer for heritage. >> i wanted to congratulate you. we've chosen to accept one of your three bids. >> the winner was mb financial, a $9 billion chicago bank. the night of the takeover, all of heritage community's branches became mb banks. mitchell feiger is mb's c.e.o.

11:41 pm

it's almost as if nothing had happened. >> almost nothing did happen. it's the same products. it's the same services. it's the same people taking care of the same customers. >> it was a sweet deal for feiger. the f.d.i.c. paid mb financial $3.5 million. mb got all of the deposits, customers, and loans. if some of those loans go bad in the future, the f.d.i.c. will pick up at least 80% of the losses. we wondered what feiger thinks of the health of banking today. >> you have to believe that dozens and dozens and dozens of more banks have to fail, but it's okay. >> what do you mean, it's okay? >> it's okay, because i think the process is smooth. depositors are fully protected by an industry-funded f.d.i.c. insurance. and i think that taking out the weak players and taking some capacity out of the industry is good--it's good for the industry. it's good for the survivors. it will produce, at the end, a much healthier banking system.

11:42 pm

>> if you can put heritage community bank out of its misery, why can't you do the same with citigroup? >> first of all, i don't talk about open and operating institutions. we can only deal with the resolution of a bank, a federally chartered or state chartered depository institution. and these very large institutions that are creating the headlines now, these are really very large financial organizations, so it's more than a bank. it's a broker-dealer. it's offshore operations. it's foreign deposits. >> we notice that while giant banks get bailed out, investors in failed community banks like heritage get wiped out. ben bernanke, the chairman of the federal reserve, says that the system is unfair for smaller banks and that's just the way it is. >> well, i think that's true. and going forward, i think we need to really review the size of these institutions and whether we should do something about that. >> bair surprised us when she suggested that maybe the mega banks, those bailed out by the taxpayers, shouldn't be allowed

11:43 pm

to exist in the future. >> well, you know, i think taxpayers rightfully should ask that if an institution's become so large that there is no alternative except for the taxpayers to provide support, should we allow so many institutions to exceed that kind of threshold. >> and the idea would be that no bank would grow so large that it posed a systemic risk to the economy. >> that's right. >> that'd be a very different world. >> it would be a different world. >> because heritage community bank was bought by mb financial, the f.d.i.c. didn't have to pay depositors. even accounts over the insurance limit were safe. for cheryl bates, it was her fourth closing this year but certainly not her last. what do you want people to think when you tell them you're from the f.d.i.c.? >> i always want them to think that i'm one of the good guys and that we want to make sure that they get their money back should their bank fail, that they are going to be okay because the f.d.i.c. is there. >> on october 19, 2010,

11:44 pm

the f.d.i.c. reported that bank failures would cost the deposit insurance fund $52 billion from 2010 through 2014. in november 2010, the f.d.i.c. filed suit against former c.e.o. john saphir and ten other executives of the failed heritage community bank. the f.d.i.c. alleged that the executives were negligent in their management of the bank's commercial real estate program, which ultimately contributed to its collapse. in a statement, lawyers for the defendants said the lawsuit lacked merit. [stopwatch ticking] coming up... does it make sense to keep making the one cent coin? >> it's unsustainable. you can't sustain losses on pennies and nickels and expect to be a viable organization that benefits the american people. >> next, when 60 minutes on cnbc returns. ♪

11:45 pm

[ male announcer ] a european-inspired suspension, but not from germany. ♪ a powerful, fuel-efficient engine, but it's not from japan. ♪ it's a car like no other... inspired by a place like no other. introducing the all-new 2013 chevrolet malibu, our greatest malibu ever.

11:46 pm

♪ at legalzoom, we've created a better place to turn for your legal matters. maybe you want to incorporate a business you'd like to start. or protect your family with a will or living trust. legalzoom makes it easy with step-by-step help when completing your personalized document -- or you can even access an attorney to guide you along. with an "a" rating from the better business bureau legalzoom helps you get personalized and affordable legal protection. in most states, a legal plan attorney is available with every personalized document to answer any questions. get started at legalzoom.com today.

11:48 pm

>> should we make cents? now, before you answer that, we're talking about those insignificant one cent pieces in your pocket or purse. it may or may not come as a surprise that it costs the u.s. mint almost two cents to make one penny and almost a dime to make a nickel. if the economy of that eludes you, join the club. even in washington, where they literally have the right

11:49 pm

to print money, as morley safer reported in february 2008, there's an ongoing debate over whether it's worth the trouble to keep making cents. >> every year the u.s. mint turns out 8 billion shiny new pennies using high-tech presses that operate faster than the eye can see, stamping out abe lincoln on blank pieces of metal. >> we're making 12 pennies per second. we're making a couple million pennies a day. >> and, says u.s. mint director edmund moy, despite inflation, despite their lowly status, 8 billion pennies still add up to... >> $80 million. that's real money. >> trouble is, to get $80 million in pennies, the government spends $134 million. and to produce 1.3 billion nickels costs $124 million, even though the coins are worth only about half that much. it's weird economics when it really comes down to it,

11:50 pm

isn't it? >> well, from our perspective at the united states mint, it's unsustainable. you can't sustain losses on pennies and nickels and expect to be a viable organization that benefits the american people. >> how did we get in this fix? >> you know, coins are made out of metal, and worldwide demand for copper, nickel, and zinc have dramatically increased over the last three years. that's what's primarily driving up the cost of making the penny and nickel. >> washington is considering ways to reduce the cost of making pennies and nickels. among them, giving the mint authority to use cheaper metals like steel. though efforts in congress to retire the penny altogether have failed in past years, its detractors say the time has come. >> inflation has rendered the penny nearly valueless, right? if you can't buy anything with a penny, if it takes at least a nickel or dime to buy anything, then that individual unit just doesn't serve much good. >> stephen dubner is the co-author of that bestseller

11:51 pm

freakonomics, a zany look at money and american culture. he puts the penny in the same category as your pesky appendix and other useless relics. >> i think that the two big reasons to keep the penny are inertia, 'cause it takes a lot of work to get rid of something that's ingrained, and nostalgia, but you need to put a price on even nostalgia. >> but is there--don't you think that there's a kind of sentimental attachment? everyone remembers their piggy banks when they were a kid, saving your pennies, and all of the old adages that go with the penny. >> "penny for your thoughts." >> "penny saved is a penny earned." >> but i would argue that, you know, in the old days you might have said, "a penny for your thoughts," as a nice kind of way of saying, "you know, whatever you're daydreaming about, it's worth something." now it's an insult. "a penny for my thought? it's only worth a penny? come on." >> what do you do with your pennies? >> well, i have kids, so i try to teach them early on not to get any pennies. i try to teach them early on to get rounded up or rounded down at any opportunity. when we play monopoly at home, we get rid of the ones and fives. it's like, it doesn't matter.

11:52 pm

>> but as fans say, a penniless america would leave the penniless truly penniless, because merchants would round prices up to the nearest nickel. mark weller is the voice of americans for common cents, a pro-penny group that claims that rounding up will cost americans $600 million a year. >> you're gonna be hurting those that can least afford it. the folks that don't have checking accounts, that don't have charge cards, are the ones that are gonna get hit. [people shouting] >> weller says, without the penny, charities, too, would suffer, on the theory that people are less likely to donate as many nickels. as it is, penny drives around the country collect tens of millions of dollars a year for medical research for the homeless, for education. >> you have school groups all over the country that are raising funds for important causes, on katrina relief,

11:53 pm

for new computers, or other issues for their schools. >> but as weller freely admits, he's got a financial interest in the high cost of penny-pinching. remember that shower of zinc pennies at the mint? well, weller's a lobbyist for jarden zinc, the tennessee company that sells those little blank discs for the mint to turn into lincoln pennies. if you don't have the penny out there, it would be a major kick in the pants to the zinc industry, wouldn't it? >> i think if you look at overall at the uses of zinc in the economy, that this is a smaller part of that overall. i think if you look back at the merits of the argument, which is, what happens if you don't have the penny and you round transactions to the nickel. that's a loser for charity groups. that's a loser for the american public. >> and on the contention that rounding to the nickel would force prices up, mint director moy says weller may have a point. >> we've taken a look at the studies of countries who have gotten rid of their lowest denomination coin. there's always at least a one-time inflationary hit

11:54 pm

upwards. >> prices have a habit of doing that, don't they? >> people are generally in the business of trying to make money. >> but the business of making money literally isn't all bad. the cost of producing most currency is far below its face value. paper money, for example, ones, fives, tens on up, cost six cents each to print. only the penny and nickel are big-time losers. the debate over the penny is one into which everybody puts their two cents worth, or call it four cents worth. >> i mean, if you ask americans, "do you want to keep or abolish the penny?" most people say they want to keep it. now, i would argue that those same people would have said they want to keep the rotary telephone, they wanted to keep, you know, carbon paper, they wanted to keep the buggy whip. but you know what? we've done all right without all those, and i think that if the penny were no longer around, people would be okay. >> americans may differ on what the utility of a penny is. i know when i go home i have

11:55 pm

a penny jar just like everyone else. but at the end, i still turn those pennies in because they're worth real money. >> you, as an amateur coin collector, i suspect you're in favor of keeping the penny, in your heart of hearts, yes? >> well, as a public official, i have no private opinions, but i do know that a lot of people are attached to the penny, and as long as they continue being in demand, the mint has an obligation to continue making them. >> in february 2010, the u.s. mint officially released a new penny into circulation which had been redesigned in 2009 to honor the 200th anniversary of lincoln's birth and the 100th anniversary of the lincoln penny itself. get rid of the penny? not likely. that's this edition of 60 minutes on cnbc. i'm leslie stahl. thank you for joining us.

11:57 pm

up. a short word that's a tall order. up your game. up the ante. and if you stumble, you get back up. up isn't easy, and we ought to know. we're in the business of up. everyday delta flies a quarter of million people while investing billions improving everything from booking to baggage claim. we're raising the bar on flying and tomorrow we will up it yet again. oh, just diagramminghey mike. this accident are you up to? with my state farm pocket agent app. you can also get a quote and pay your premium with this thing. i thought state farm didn't have all those apps? where did you hear that? the internet.

11:58 pm

and you believed it? yeah. they can't put anything on the internet that isn't true. where did you hear that? [ both ] the internet. oh look. here comes my date. i met him on the internet. he's a french model. uh, bonjour. [ male announcer ] state farm. more mobile than ever. get to a better state. has a lot going on in her life. wife, mother, marathoner. but one day it's just gonna be james and her. so as their financial advisor, i'm helping them look at their complete financial picture -- even the money they've invested elsewhere -- to create a plan that can help weather all kinds of markets. because that's how they're getting ready, for all the things they want to do. when the conversation turns to finding a financial advisor who's fully invested in you, turn to us. wells fargo advisors. together we'll go far.

165 Views

IN COLLECTIONS

CNBC Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on